Managing Chargebacks

When a chargeback occurs, BlueSnap will notify the merchant via email or the Chargeback webhook (if webhooks are enabled for your account).

BlueSnap has partnered with Chargebacks911 to provide you with the capability of monitoring, accepting, and representing (fighting) chargebacks. You can also access impactful reporting and analytics in the Chargebacks911 portal.

Retrieval Requests

We recommend that you respond to all retrieval requests. A response to a retrieval request doesn't guarantee that a chargeback won't occur, but it might stop a chargeback. In many cases, the cardholder does not recognize the transaction, so providing basic transactional information can sometimes be sufficient to end the dispute. Not responding to a retrieval request might impact the merchant's rights to contest a chargeback.

Managing Chargebacks

You can manage chargebacks on your own, or you can choose to have our team of professionals handle chargebacks on your behalf. Learn more about dispute management service levels here.

Note: If you are the admin user of the BlueSnap account, the Chargebacks911 portal opens in a new tab. If you are not the admin user, please contact the admin user of your company's Chargebacks911/ BlueSnap account to obtain your Chargebacks911 login credentials.

Israeli Chargebacks

CB911 does not support transactions processed by local Israel acquirers. In case of a chargeback, we send an email notification. We strongly recommend that you enable the Chargebacks email notification so you can dispute chargebacks as quickly as possible.

To manually dispute a chargeback that is not visible in the CB911 Dispute Portal, complete the online dispute form. Below are some document types that you can attach to the online dispute form:

- Copies of invoices.

- Signed cardholder agreements. Electronic confirmation is also acceptable.

- Proof that the goods were delivered and services were rendered.

- Proof that shows the cardholder authorized the transaction (Valid AVS and/or CVV capture).

- Previous transactions not disputed by this cardholder (if applicable).

- Proof that 3DS was used to authenticate the transaction (if applicable).

- Digital proof of usage, including device-identifying data (if applicable).

Pre-Arbitration / Second Chargeback

Responding to a pre-arbitration case is risky and not recommended, even if you have additional evidence. Pre-arbitration cases decided in favor of the shopper can result in the card network assessing fees of $500 or more, in addition to any fees they've already paid out during the previous stages. Since responding to a pre-arbitration may result in high fees if the merchant loses and the likelihood of a merchant winning is low, BlueSnap does not recommend or support responding to a pre-arbitration case.

Monitor a Chargeback

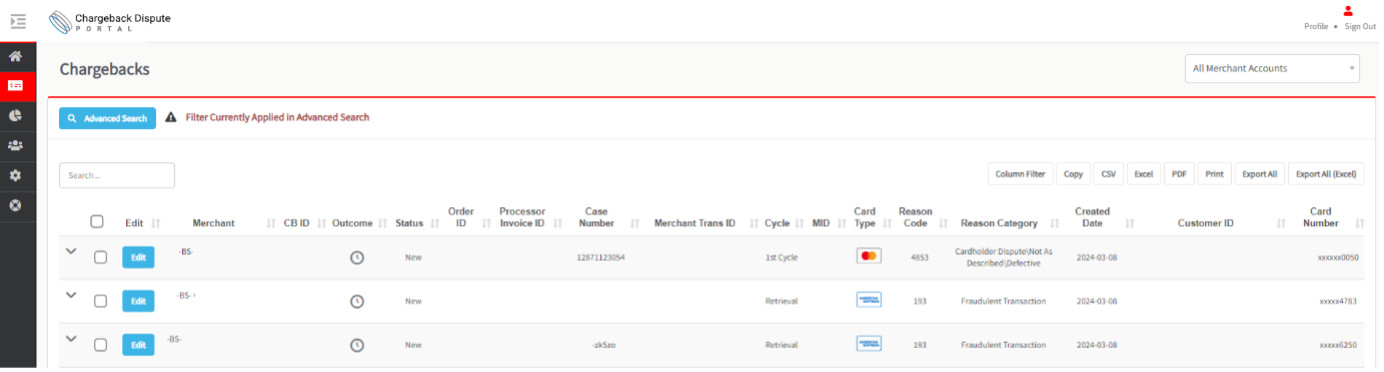

To access the Chargebacks911 portal, log in to BlueSnap's Merchant Portal and select Chargebacks in the left-hand navigation menu.

Once you log in to the Chargebacks911 portal, click Chargebacks in the left-hand navigation panel, and then choose Chargebacks again from the options. This portal area shows details for each chargeback at every stage of the chargeback life cycle, including the associated payment identifiers, the chargeback amount, the response due date, and the reason for the chargeback. You can use the advanced search parameters to adjust the data you view; search for a single chargeback, chargebacks from a specific card type or a particular reason code, or download all your chargeback data in CSV, Excel, or PDF format. This area is informational only; all the action happens in the Case Management area.

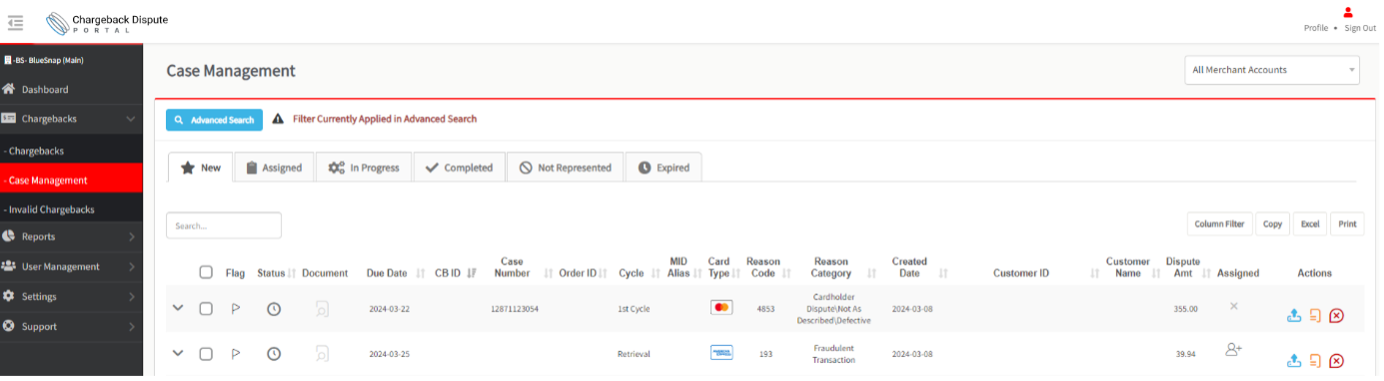

Click Chargebacks in the left-hand navigation panel, and then choose Case Management from the options. This area of the portal allows you to perform critical actions. You can assign chargebacks to your team members, accept or fight new chargebacks, and view the status and outcome of chargebacks you disputed.

Accept a Chargeback

By accepting a chargeback, you acknowledge that it is valid and that the shopper should get their money back, which may be the best option when:

- The chargeback reason is legitimate, e.g., a fraudulent transaction.

- The chargeback amount is too low, or the effort required to respond to the chargeback is not cost-effective.

- Sufficient evidence compelling enough to successfully challenge the chargeback is not available.

Prioritize and Select Chargebacks to Represent

It's best to prioritize representing chargebacks that allow you to recover as much revenue as possible. Considering the following criteria:

- The underlying transaction is valid, and the chargeback amount is high enough to make the process cost-effective.

- You have enough compelling evidence to overturn the chargeback, or you have proof of a refund before the chargeback. Always dispute chargebacks when you previously issued a refund to a customer to avoid being debited twice the disputed amount.

Important Notes

- You should always respond to a chargeback on a previously refunded sale with proof of the refund and a description of how the refund is related to the disputed charge.

- Disputing a chargeback does not guarantee that the issuing bank will resolve the chargeback in your favor.

- BlueSnap does not decide chargeback outcomes. The shoppers' issuing banks determine the results, following rules and regulations set by the card payment brand.

- You should never refund a transaction after a chargeback is received. You could lose both the chargeback and refund amounts.

- You are required to respond to chargebacks you choose to represent by the Due Date displayed in the Case Management area of the Chargebacks911 portal. Responses are due approximately ten days after the chargeback was created (3-4 days for chargebacks from Latin America). Once a chargeback has expired, you will lose the ability to respond to it. If you decide not to represent the chargeback or should you fail to respond in the time allotted, you will automatically lose the chargeback, and the funds will remain with the shopper.

Representing Chargebacks

By representing a chargeback, you are telling the issuing bank that you believe the shopper's claim is invalid and have evidence strong enough to prove it. You should tailor evidence to address the chargeback's reason code. Visit Representing Chargebacks for our complete guide to representing chargebacks and a detailed list of the recommended evidence for each card brand, product type, and reason code.

Resolution

After you represent a chargeback, the next step is for the issuing bank to review any evidence that you have submitted and deliver a verdict. BlueSnap will update the outcome of the chargeback accordingly in the Chargebacks911 portal:

- If the issuing bank agrees with your assertion that the chargeback is invalid, the portal will display the outcome of Win in the Chargebacks911 dashboard, and BlueSnap will make a credit adjustment to your account.

- If you choose not to fight a chargeback, or if the issuing bank decides your evidence was insufficient, the Chargebacks911 dashboard will display an outcome of Loss, and the funds will remain with the cardholder.

Pre-arbitration/second chargeback cases are reported separately in the Chargebacks911 portal. A chargeback with two records, one with the outcome Win and another with Second Cycle in the Cycle column, should be considered a net loss, as the issuer decided this chargeback in favor of the cardholder in pre-arbitration.

Note: It can take up to 120 days for the issuer to deliver a final verdict on your representment.

Updated about 1 month ago